The main reason 401(k) contributors propose a Roth IRA conversion is to limit their tax liability in retirement. The only problem is, the conversion process costs more headaches and tax implications in the end, unless you are unemployed or in a low marginal tax bracket.

A 401(k) and Roth IRA are both tax-advantaged investment saving accounts. The funds are designed to be withdrawn in retirement. A 401(k) is an employer sponsored retirement plan where an employee contributes as much as they can per year, hopefully the max as a portion of their income to save up for retirement using pre-tax dollars. The maximum 401 (k) contribution rate for 2021 currently stands at $19,500k and $20,500 for 2022 as it increases by roughly a thousand each year. A pre-tax account is tax deferred meaning the contributions grow tax free until withdrawn.

On the other hand, a Roth IRA is not provided by an employer and instead an investor themselves must open it through a brokerage, similarly to a traditional IRA or any other savings account. A Roth IRA is most appealing due to its perks of being a post-tax account where contributions are taxed pre-deposit and are withdraw tax free. A Roth IRA can be used to fund for retirement or for any other needs after 59 ½. The account also must be at least 5 years old.

Luckily if you need the funds earlier, unlike a 401(k), there are qualifying exceptions that allow you to use the funds without incurring a hefty penalty.

These qualifying exceptions include:

-First-time home purchase a.k.a downpayment

-Need money for disaster recovery

-College expenses

-Disability and extra aid

Otherwise you incur a 10% withdraw penalty + taxes.

If you are in a high-tax bracket and looking to skip out on paying as much tax as possible, it would’ve been best to fund a Roth IRA when you were younger since a conversion today would require you to pay income tax on top of your adjusted gross income which doesn’t make sense.

Since one can only invest up to $6k in a Roth IRA in 2021, this is the most advantageous plan for those earning a lower income since they are placed in a lower tax bracket. Roth IRAs are most advantageous for students and young professionals starting out who can already start building their nest egg for retirement and get taxes over with earlier than later on heftier gains.

A Roth IRA and 401(k) are just investment accounts geared for retirement but the major distinction and priceless asset a Roth IRA carries is that it’s a POST-TAX account.

Conversion What?

These plans are confusing enough. With only 32% of Americans invested in a 401(k) and only 10% owning Roth IRAs, conversions aren’t a popular consideration for most Americans but should be since those who don’t earn much would gain the most from it.

Let’s say you have always been financially savvy and have a knack for making money. You opened up a Roth IRA once you started earning your first buck in 5th grade at the ice cream parlor. Along with the bank of mom and dad, you helped fund it to the max each year with various side hustles which allowed you to build a comfy stable retirement fund as a teenager, with more funds than what middle-aged Americans on the brink of retirement have saved up.

You now have graduated college and are working for a large private enterprise. You are immediately enrolled in a 401(k) and contribute to the max each year. Slowly but surely within a few years, you rise the ranks of the corporate ladder and are officially earning a top 10% salary, over $280k per year. At this point you aren’t qualified to contribute your earnings to a Roth IRA since it is over the earned income limit for a Roth IRA currently phased out at $125k for singles but you still want to take advantage of the compounding magic it offers.

This is where the conversion comes into play and when it should also NOT be considered.

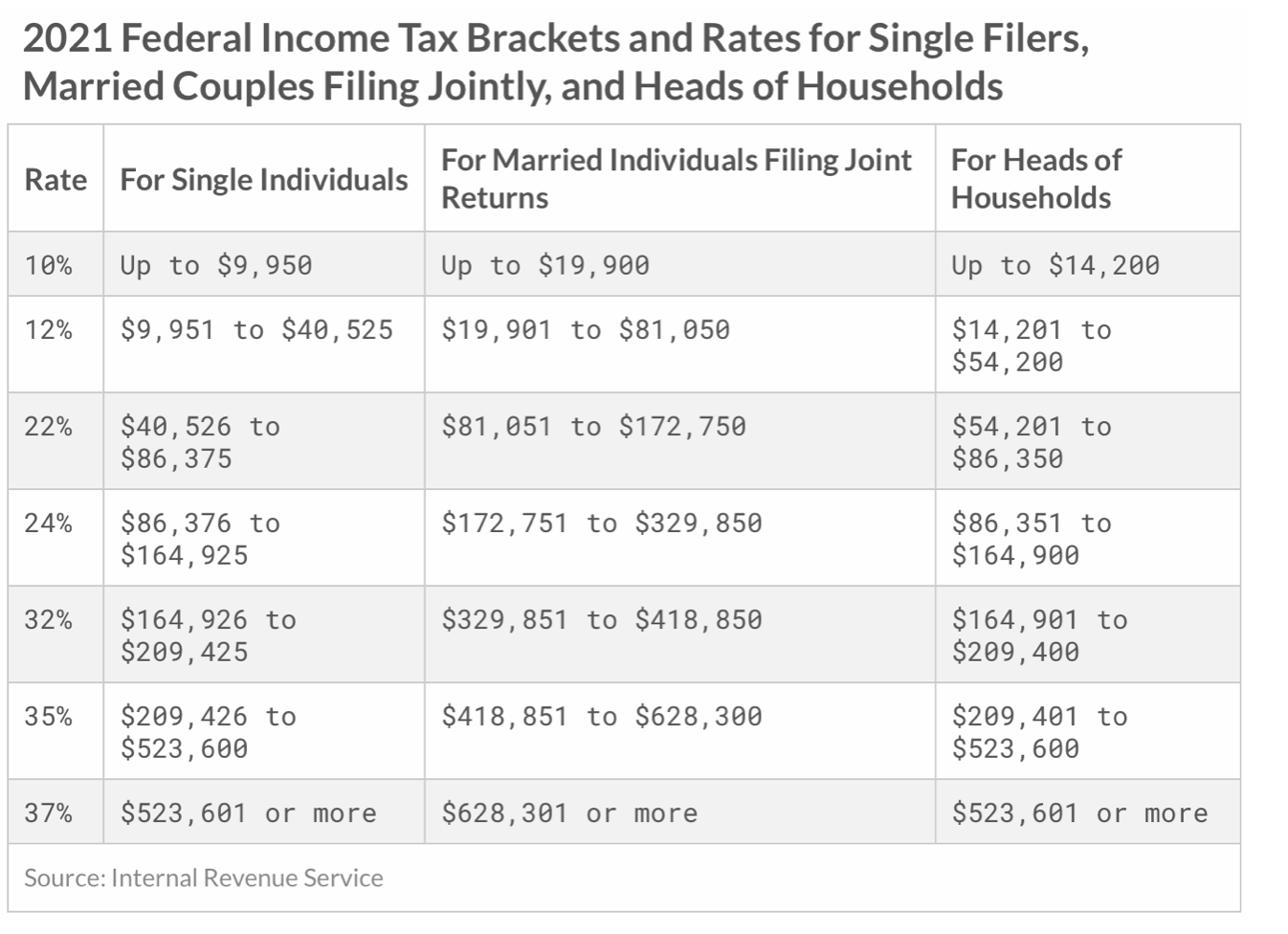

In this scenario, earning over $280k puts you in a moderately high tax bracket as a middle class and above earner. If you were to convert your 401(k) funds into the Roth IRA to skip out on paying taxes in retirement and instead now, you would be paying a whooping 30%+ income tax on-top of your AGI due to your high-income. The conversion would only make sense if you reduced your earned income and were planning on retiring sooner than later so you can pay as little tax as possible.

A conversion sounds fancy and like another legal loophole but in hindsight it’s not worth it.

Why Post-Tax vs Pre-Tax Is A Big Deal

As Benjamin Franklin pronounced, “In this world, nothing is certain except deaht and taxes.”

Billionaires and everyone alike each year strive to find any possible way to skip out and pay less tax. Hopefully in a legal way.

Why?

We believe we deserve what we earn and should keep every penny. The more one earns in W2 income from an employer, the more they have to give back to the gov’t while a business owner who has no pay ceiling or boss can earn double what they earn as an executive and pay little to nothing all thanks to the power of depreciation, tax-write offs, Section 1031 tax code, and earning different forms of income that are more tax advantageous.

Just like unrealized gains in one’s portfolio aren’t taxed only until a profit is made from a sale through capital gains, portfolio and passive income aren’t either, only earned income robbing the poor and middle class exacerbating wealth inequality further.

When you look at each individual on the Fortune 400 Wealthiest Americans List, all of these people head some sort of business. Whether it’s rental properties, gas stations or a public company, they don’t work for someone else which allows them to keep more in return. I’m not saying that they didn’t in their prior life, I’m sure they did to get a head start and build momentum from there, but to sustain their influence, power, and most notably wealth today, they had to diversify their income streams in tax-advantaged ways which works best through investments and physical tangible assets.

Not only increasing your portfolio and passive income streams will help one rise the socioeconomic ladder, setting up a Roth IRA is a core part of this equation as well. Sure having a brokerage account is ubiquitous amongst the elite since investing in the markets is by far the easiest way to grow your wealth and not be burdened by a pay ceiling, physical labor or your time, but starting as early as possible with a Roth IRA as a kid is by far the best way to compound your wealth overtime.

I’m sure Benjamin would have agreed with Buffett on his statement that “compounding is the eighth wonder of the world.”

This phrase directly correlates to the power of a Roth IRA and no other account.

You may be asking, well doesn’t every investment account compound in some way?

Well, if you own diversified index funds and ETFs that track a broader index, yes, but if you are overly aggressive and hold onto mutual funds that are actively traded, not always.

A Roth IRA is designed to be a long-term fund. Just like a 401(k), IRA, SEP IRA for small business employees, 457 for non-profit employees, and the list goes on, all these plans are designed for retirement and not to be used today.

Retirement is by far the most expensive and scariest part of one’s life and must be planned for as early as possible. Never be ashamed to start planning for retirement at the golden age of 20. You’ll thank me later when the dollar drastically depreciates in 60 years.

A Roth IRA isn’t magically going to provide you any more stability than a regular brokerage account but it will boost your contribution potential. It’s as important as maxing out your contributions to your 401(k) which currently stands at $21k in 2021 and only increases each year!

It is also a popular tool for estate planning purposes as contributors don’t have a required minimum distribution amount meaning that if you don’t need the funds in your lifetime, heirs/beneficiaries can draw the money tax-free skipping probate. Similarly to a 529c they can be passed down to beneficiaries and continue to grow forever!

Roth’s Rule

The Roth’s true power over any of these accounts is that it can be opened as soon as you are born even when you aren’t earning income! Majority of Roth IRA’s contributions should be composed of your earned income but most people don’t know that children as young as they can physcially start working can earn as well through their parent’s business.

The contribution limit is only $6k for a reason and there is no age min. It is made for low-income earners to start building their wealth early and funds cannot be withdrawn until 59 ½ since it is made to be a long-term account.

High-income earners cannot open or contribute to a Roth IRA due to this income restriction. As of 2020, if you make less than $125,000 as an individual or less than $198,000 as a married couple, you can contribute the maximum $6,000 to a Roth IRA.

If you are in a 32% or higher tax bracket, a Roth IRA conversion requires you to pay more tax dollars on top and below that bracket, the breakeven point, a conversion won’t even make a difference.

The lower the tax bracket you are in, the more bang for your buck you will get from the Roth IRA since you get to grow that money tax free forever. If you’re earning over $139k as an individual and want to contribute half of that to a Roth IRA, you will have an unfair advantage once you withdraw funds at 59 ½. High earners lie in a higher tax bracket for a reason and don’t have the same privileges as lower-earners do in terms of a Roth IRA but as long as you are maxing out your 401(k) and following the basic budget principles of financially free and flexible individuals, you are setting yourself up on the right path.

These practices include but are not limited to:

-Not depending on anyone except yourself

-Never spending more than 20–40% of your net worth on a home

-Striving to save at least 50% of your income to reinvest back into the markets, your 401(k), health insurance, and other needs

-Buy what you need, not what you want

-Invest in alternatives

-Have several brokerage accounts

-Emergency stash cushion of at least 20% of your net worth in cash at all times

-Save and invest aggressively not tempted by stuff you odn’t need ot impress people you do’t know

-Limiting ‘toxic’ liabilities as much as possible and appropriately paying off debt as soon as possible

How to Get Started With A Roth From Birth

The answer we’ve been waiting for.

Although only earned income can be invested into a Roth IRA, you can pay your child with helping you with your business (real estate property, LLC, blog, construction service, etc.) and invest up to that amount. If they are able to take on any job when they are younger, more power to them but with a business, you can hire them as a model, assistant of some sorts, you name it and you can contribute that ‘earned’ income, usually tax-free since it’s not W2 income. No matter where it comes from, if it’s earned, it’s for the Roth.

When your child is born, there’s already enough to handle. From health insurance to schooling, playdates to schedules, a Roth IRA is the last thing on parents’ minds and tends to be something they push on the side until their child goes to college or graduates already on their own.

The average age one starts earning their first paycheck is at 16. This makes sense since federal chid labor and several state laws have placed the minimum working age to 14.

But that shouldn’t stop a parent or their child from opening a Roth IRA. Although it is recommended to gain working experience as early as possible since the real learning starts outside of the classroom, it’s not necessary to open an account thanks to parental assistance.

If parents are able to, they can start funding their child’s Roth IRA by hiring them themselves.

I believe this is the gift that truly keeps on giving.

This is set up by opening a custodial Roth IRA. Since a child is a minor until age 18, the Roth IRA would be in the parents’ name and have full custody.

Fortunately, my parents prioritized my finances before I was born which allowed me to build my nest egg early on and be independent at age 18. After all, having a child is expensive in itself and keeping the finances in order is a key accelerator to financial freedom. They had not only set up a 529 account for educational expenses but a Roth IRA as well which were all discovered through books in the early 2000s. I’m extremely appreciative of this, especially since I was born on Thanksgiving!

Beyond that point, I had contributed to the funds myself once I started working at age 13 in various gigs from modeling to tennis coaching, babysitting to IT help assistant, and so on and so forth.

The Roth IRA has been by far the greatest propellent to my wealth and a true gift encouraging me to work and fund my own lifestyle.

Of course, a Roth IRA to a 401(k) are investment accounts and still come with volatility, risk and uncertainty, the three certainties in the market. Yet if you stick with an appropriate risk tolerance and look towards the long-term, you are in a good place.

Why A Roth IRA Conversion Is Not Worth It

If everyone could turn back time and open up a Roth IRA earlier than later, they would. Sadly only 10% of Americans have one. Hopefully that number increases once this article publishes. If high earners could contribute to their Roth IRA, they would choose it over any other retirement plan due to the massive tax-advantages of withdrawing the money tax-free! It feels liberating to do so.

The obvious time to do a conversion is when you are in the lowest tax bracket of your life. If you can forecast your tax rates and believe you may want to take a gap from work and live off your severance for a while, this is a better time to convert as your marginal tax bracket will decline but once again, it’s not necessary to convert at all. You pay tax either way and save very little in the process.

Since roughly 10% of Americans only have $1 million or more saved for retirement according to TD Ameritrade, it makes sense to convert to a Roth IRA once you are retired as you collect social security benefits and start withdrawing from your traditional IRA anyways, preferably at a 4% or so withdrawal rate.

Also, did you know that your Social Security income isn’t fully taxed either? The gov’t is always here.

Wonderful But Worst Case Conversion Scenario

Let’s say you’re earning a top 1% income. Congrats! This means you are earning at least $500k per year and also giving away 37% of it to Uncle Sam. You’re dying to contribute to a Roth IRA due to massive guilt of not starting earlier but refuse to lower your income.

Although earned income is the main source for Roth IRA contributions, here are some additional ways to lessen your tax burden outside of it:

-Start a business, LLC, enterprise, blog, manage a rental property-negative or positive cash flow doesn’t matter as long as it generates passive income with qualifying expenses

-Move to a more tax-efficient state such as Florida where there is 0 income and state tax. Be neighbors with the billionaires!

-Donations and involved in charitable giving for a tax deduction

-Setting up an estate plan to avoid probate, unnecessary taxes and fees

-Hold never sell

-Withdraw when you are in a lower-tax bracket for a 401(k)

-Invest in non-income producing investments such as dividend paying stocks or bonds that pay interest

Overall, the best time to do a Roth IRA conversion is when you are in the lowest tax bracket of your life. Even if you are unemployed or underemployed, it doesn’t mean your tax bracket will be lowered. It all depends on the current tax rates and what you’ve been earning recently. It doesn’t immediately drop once you stop. Tax rates go up and down with each new administration. No matter how much passive income you are earning, it doesn’t help since you can only contribute earned income after all.

If you can contribute to a Roth IRA, do it now. Highly speculative investments are great additions to a Roth as it is a portfolio with a long-term outlook.

If you know you will be taking retirement seriously and earning less, that can be the opportune time to do a conversion. Take advantage of tax-advantaged accounts while you can! Tax rates are only going up, especially for middle-class earners.

For the small percentage of those who were debating a conversion from a 401(k) to a Roth IRA, I hope this helps.

For the rest, continue investing more, spend less.