Decades before I was born and in the early 2000s, those who mainly traded in the stock market were mostly white collar middle aged men who went to prestigious business schools thrown into the stock market by their dad and grandfathers and head of the household as the main breadwinners.

Although today the average American only has 1–2 income sources, back in the 20th century, it was surprisingly identical even amongst the top 10%, almost all who were considered investors.

Their sources of income included:

-80–90% of their wealth built into their property (dangerous especially during the ’08 housing crisis)

-Possible inheritance from family business and in that case it usually was the only income source (also dangerous since too much money messes with our minds with no sense of purpose)

-Earned income from their 9–5 job to support the family since wifes typically didn’t work until the 70’s and really picked up in supporting the family in the 80’s

-The good old selective stock market

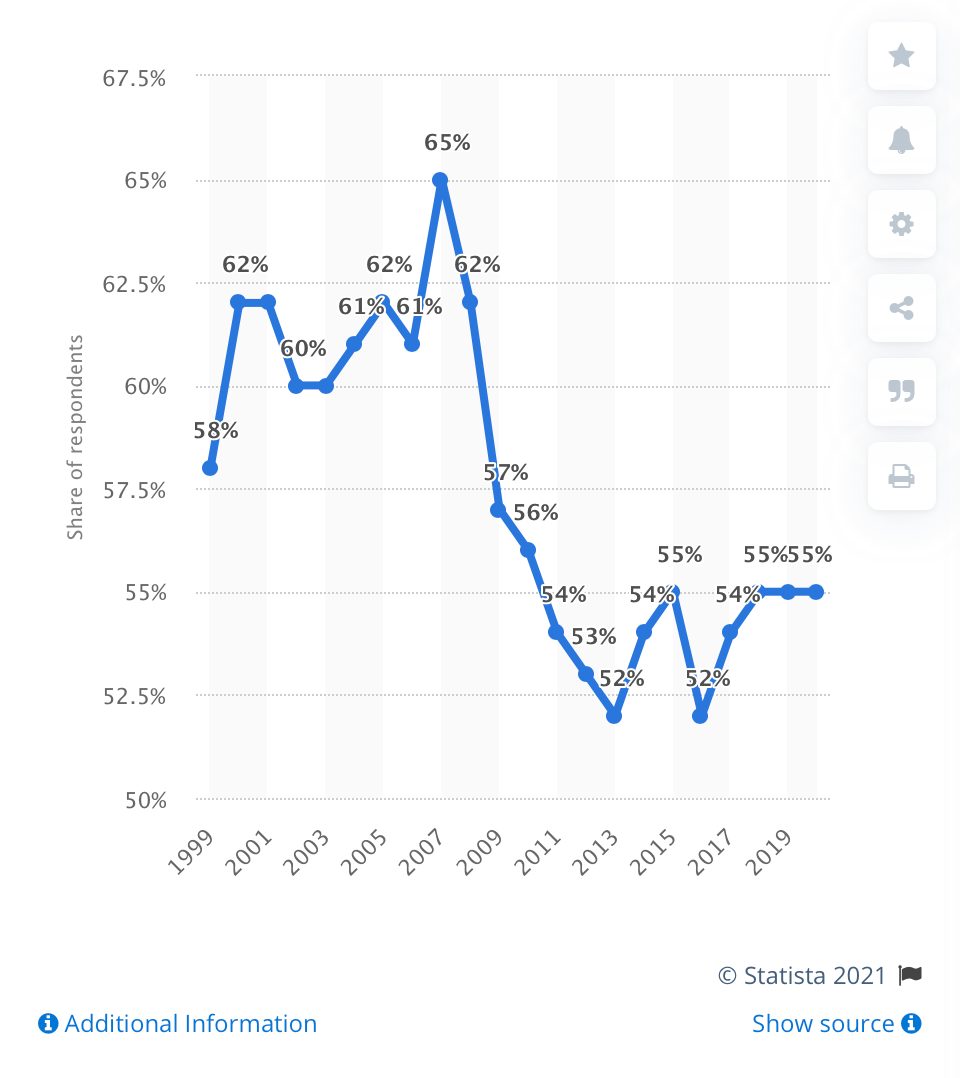

Market Share

So how did the stock market start to pivot from exclusivity to now 55% of adults in the US taking part?

Strangely although the figure has remained steady over the last few years, this amount is still far below the levels before the Great Recession when the stock market peaked in 2007 at 65% and the rich who were making money off of the market were skeptical about getting back which influenced more diverse and younger demographics to avoid it all together.

In addition to the Great Recession which was one of the worst financial collapses in modern history, a significant number of people assumed investing was about individual stock picking and took a lot of work which lead them to avoid it all together.

Not only was there no financial literacy and money was banned from every conversation, long-term investing towards goal setting wasn’t necessarily the approach investors took since most people didn’t live past 70, 80 years old.

The most popular and largest asset classes of all time are equities and derivates. Investors in the early 80’s to 90’s pointed to individual stocks and the ones they were familiar with which were not always recommended just ‘hot’ at the moment. They stayed away from gold bonds and savings accounts which lead them to take an active leveraged approach instead of long term which is now highly recommended for any risk tolerance.

Front Door

Back then, the way most investors got into the market was usually in part by working in the finance sector. Although money should never be an excuse when it comes to investing since you don’t have to have thousands to start out with, these individuals were already wealthy due to inheritance, taking the time to learn about their family’s practices in the market, earning lucrative salaries in a top industry, spending father and son time to record the daily close on paper-since most investors were men and performing all the evaluation and analysis on their own time.

There was no such thing as the Bloomberg Terminal, Yahoo Finance, Reddit or other sources to get this information from which also lead skeptical investors to simply stay away and rely on their single job to keep them afloat.

Housing Bubble

After witnessing the significant one-day losses in the stock market during the Financial Crisis, many investors turned to more alternative resources for stability and investments with longer maturities. As shown in the chart above, although the drop was significant around only 56% of Americans were invested at the time, more than today, this decrease lasted long, eventually got quickly worse and hit a trough in 2013 to only 52%.

The Truth

Frankly if you ask a random group of people today on the street if they have holdings in the market and if so what are they, they will most likely tell you random individual stocks like 1k shares of Tesla or Bitcoin. Barely anyone will give you the answer: a Vanguard low-cost index fund that tracks the S&P500 and not even know what the individual stocks that make up that fund are.

That’s the true differentiator between an active and passive investor. Those who are patient, diligent, don’t jump the gun and tie their emotions or over-leverage with stocks always win in the long term while also doing less work.

It’s a win-win situation but most people either become day traders or don’t bother at all with the market, in part due to lack of financial literacy.

As a student, this is an issue I advocate for. It is upsetting as the cost of college goes up and student loans skyrocket, more and more graduates are left stranded.

9 out of 10 millennials are in debt and have gone through 2 recessions, the Housing Crisis and Covid.

With inflation and interest rates rising, this means bonds are more expensive and harder to pay off.

It’s becoming less attractive to borrow as the 10-year bond yield slowly inches to 2% but has to be taken out regardless by students for that degree in hopes of a better life.

So is it the colleges’ fault? You can find out here who to blame for the rising costs.

With too much ‘fake news’, retail trading platforms attempting to democratize finance and social media not making sense with no regulation, this has lead bored Reddit users and GenZers + Millennials to get into the hype they never needed to dip their toes into in the first place.

They want to be attracted to whatever can get them rich quick without understanding what the heck they are doing.

This is the danger zone that prior generations in the stock market didn’t have exposure to.

How To Really Invest

Hence the name, PERSONAL finance, there’s no secret sauce to investing in the stock market because we all have our own personalized approach which can also lead to intimidation at the start.

First understanding your risk tolerance: conservative, moderate or aggressive (90–100% equity exposure = more risk = more reward or the opposite), short/long term goals-when planning on withdrawing or selling fund and how much cash is needed on the side, age-younger can take on more risk, nearing retirement-take on less to rely on returns instead of having them as another income source is all key to getting started.

To become a good investor in the market is easier than most think that’s why the youngsters are going into insurmountable amounts of debt, committing suicide (read here why) on Robinhood and buying on margin more than they could ever afford.

The stock market was never regulated until 1933 when the SEC, Securities and Exchange Commission, a gov’t agency that confirms the markets work efficiency, halts any trades if there’s too much volatility, checks in with businesses to make sure they are following regulatory policies, regulate IPOs and monitor if there is no insider trading going on even though it seems like it’s happening more than ever these days just on a different scale.

Although I’m sure FOMO, emotions and panic selling along with speculation and overvaluations on companies were happening when the stock market was reserved for those in the business world before I was born, now with the adoption of technology and social media it’s gotten far worse and influenced by the wrong people.

What’s Next With Control

I doubt retail trading platforms like WeBull, Robinhood or even institutionalized decades old brokerages such as Fidelity, Vanguard and Charles Swab will put limits on those who can and cannot trade and give a quiz on what they know.

This is far by the most competitive game on earth that everyone wants a stake in.

So why is it easy to get into but hard to earn through?

Besides needing unwavering commitment and patience the stock market is:

-Highly competitive

-Very Analytical

-Intuitive + Realistic + Futuristic

-Unemotional and Realistic

-Required to block out the noise

As a result, most retail traders (teens and Millennials) don’t have that capacity.

To become a good investor and get into the markets, here’s what needs to be checked off before stepping in in order NOT TO LOOSE:

-A list of potential investment ideas

-Estimates of their intrinsic values

-A sense for how their intrinsic values compare with their prices

-An understanding of the risks involved in each

-An understanding of how each investment correlates with each other

-Best investments usually found in misunderstood sectors such as undervalued stocks, defensive, cyclicals and blue-chip stocks that are simple and underpriced

Today’s Mania

Bored at home, many people (amateurs, students and broke college students) are turning to a new game: the stock market.

Don’t get me wrong, it’s terrific that 2020 was an epic year for individual investors as they made up an estimated 19/5% of US equity trading volume, a jump of over 4% compared to 2019 and doubled since 2010.

Although not as high as pre the Housing Crisis and the Great Recession, this has allowed people to understand how to spread their assets and not rely on one single income source. The pandemic couldn’t have come at a better time to reinforce how vital it is to have a nest egg, cash cushion and learn the basics about saving and spending.

The problem with the stock market is that it’s easier than ever and you can spend more than you physically own. With stock picks discussed across social media platforms these days this is a familiar act the same way internet stock spikes were proliferating in message boards leading up to the burst in the dot-com bubble in the late ‘90’s not correlated with traditional valuations.

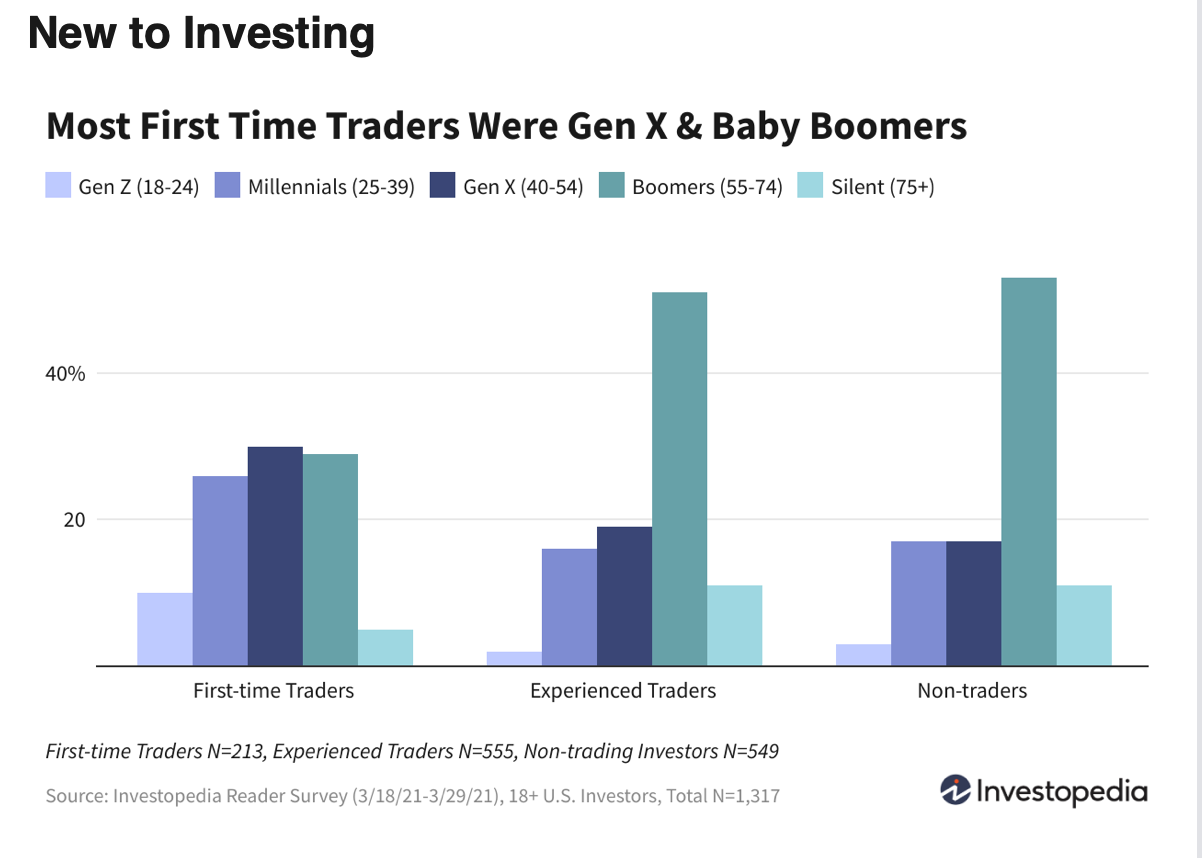

So Who Are These Amateur Newcomers?

Strangely, the millions of new investors and traders who joined the stock market in the past year may not be who the majority of financial media think they are. According to Investopedia’s recent survey of its daily newsletter readers, nearly 60% of those who said they just started trading in the past year are between 40–74 years old!

Most of the 1,300 respondents to the survey describe themselves as self-taught with 47% saying they use websites and books to educate themselves about investing and trading.

33% say they learn form their financial advisors

6% say they learn form Reddit online forums

5% social media including TikTok and Twitter

A little over half of these investors and traders admit to knowing nothing about investing before starting.

49% have little capital at risk with $50k or less invested

19% invested 500k

86% of respondents which include both new and experienced investors claim to have made gains in the past year while 53% suffered losses.

Only way to loose during a bull market is by choosing individual stocks, something to avoid all together rain or shine if you want a guaranteed return.

Factors

As millions of unemployed Americans received their stimulus checks second time around this year, this is also the main reason why people are willing to find a method to replace their lost income, even though they don’t bother investing in themselves which would allow them to see bigger gains.

Not only you need to predict the company’s performance and moves at the right moment to capitalize on fluctuations in price, it is pure gambling not investing and as a result, investors don’t realize that losses are more common than gains in this type of behavior.

Focusing on news and this digitized hype world is a problem. They don’t have time to read just watch a headline and make a move.

In the long run, those who’ve selected and own around 30 stocks only have a 40% chance of doing as well as the overall market anyway.

Over the last 31 years through 2017, the overall market was up more than 2,000%.

The median stock? Just 7%.

The only way to make sure you own the winners is to own everything.

The stock market doesn’t care who you are but will reward you for playing the long game.

If you’re curious how your fellow Americans spent their stimulus check it out here.

All I’m going to say is that I hope you join the right crowd.

Happy investing.